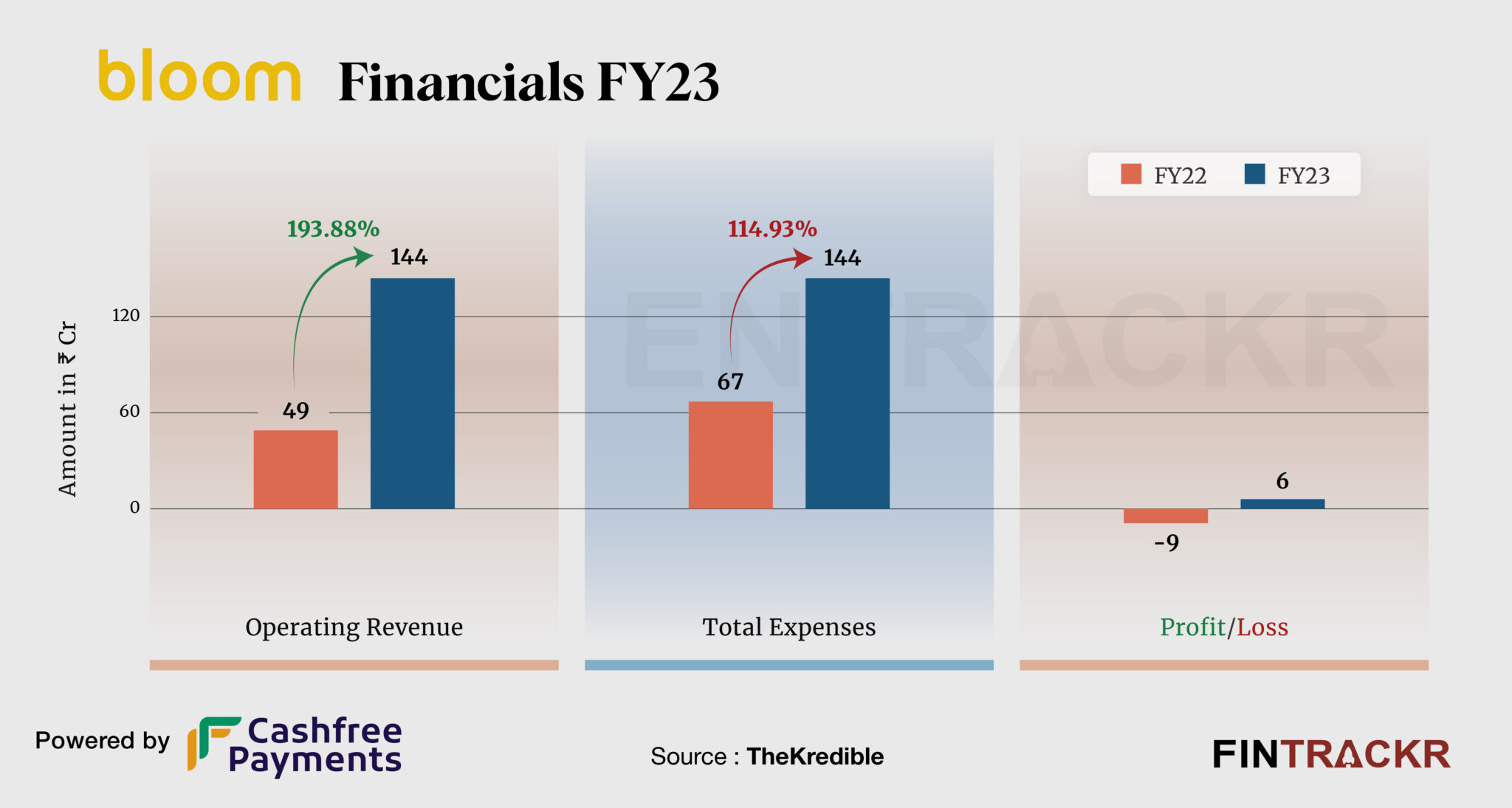

Bloom Hotels’ revenue from operations surged 2.93X to Rs 144 crore in FY23 from Rs 49 crore in FY22, its standalone financial statements filed with the Registrar of Companies show.

The company manages a diverse range of hotels, namely Bloom Hotel, Bloom Hub, BloomSuites, and Bloomrooms. Currently, it has over 50 hotels located across Mumbai Pune, Udaipur, Jaipur, NCR et al. The income from the sale of accommodation formed 83% of the revenue which surged 3X to Rs 119 crore in FY23. The rest of the collections generated from the sale of food and beverages and allied services.

For the hotel chain, the cost of rent and leasing accounted for 30% of the overall expenditure which shot up 152.9% to Rs 43 crore in FY23 from Rs 17 crore in FY22. Its employee benefits and consumables saw a surge of 81% and 143% respectively in the last fiscal year. Bloom Hotels’ advertising, commissions, legal/professional, and other overheads increased its total expenditure by 115% to Rs 144 crore in FY23 from Rs 67 crore in FY22.

Expenses Breakdown

- Cost of material consumed

- Employee benefits

- Rent

- Power and fuel

- Advertising promotional

- Commission

- Others

To check complete Expense Breakdown visit thekredible.com

The three-fold surge and controlled cost mechanism helped Bloom Hotel to turn itself profitable with Rs 6 crore profit in FY23. The company recorded a loss of Rs 9 crore in FY22. Its ROCE and EBITDA margin registered at 3% and 8.6% respectively.

On a unit level, it spent Re 1.00 to earn a rupee in FY23.

| FY22 | FY23 |

| EBITDA Margin | -8% | 8.6% |

| Expense/₹ of Op Revenue | ₹1.37 | ₹1.00 |

| ROCE | -4% | 3% |

Bloom has been careful to nurture its image as a small yet quality option for travelers. Be it the choice of relatively upscale locations, or the amenities offered, the chain has rarely pushed for, or promised anything where it risks falling short. However, the possibly higher satisfaction of its guests can only deliver so much on a small base. Thus, the chain faces the task of scaling up without compromising on quality, something that all of its peers have struggled with at various times. With a sharper, more well defined template, we believe Bloom has a better chance than most of making it. It seems very likely that FY24 numbers will be healthy for this chain, and set the base for the next level of growth to 100 properties.